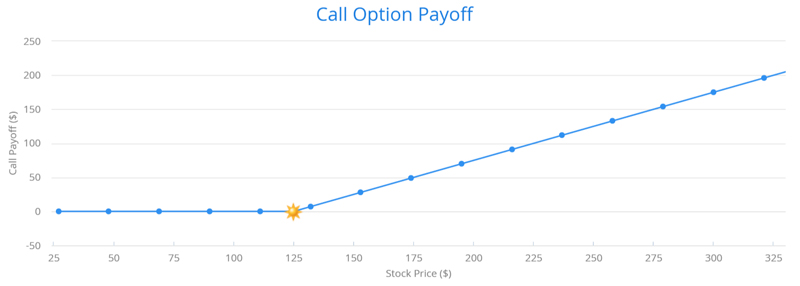

Valuation of Stock Call Option

The owner of the European stock call option with exercise price P and maturity of n months has a right to purchase the underlying stock for price P in n months from now. The payoff chart below describes the cash flow that the option owner will receive in n months from now. If the price of the underlying stock is less than or equal to P then the option owner will receive zero cash because the owner, being a rational investor, will not exercise his right to buy the stock for P since the stock could be bought on the market for less than P. If the price S of the underlying stock is greater than P then the option owner will receive positive zero cash flow – the option holder could buy the stock for P and then sell the stock for S, realizing the profit equal to S-P . In the latter case, the greater the underlying stock price the greater the proceeds received by the option owner since the option owner can buy the stock for a fixed price P.

While it is easy to determine the value of the option at its maturity when the price of the underlying stock is known it is much harder to estimate the present value of the option when there is considerable time before the option expires and the price of underlying stock varies as influenced by the market. Fortunately, the intellectual giants that came before us managed to solve the problem. The Black–Scholes formula gives an estimate of the price of European-style options. More importantly for our case, there are numerical methods, such as binomial trees, that can be used for estimating the present value of the derivatives where derivatives payoff functions are more complex than payoff functions for European stock call options and where the derivatives rights could be exercised before the derivative maturity/expiration.